Routing Transit Number: A Guide To Its Importance And Usage

Understanding the routing transit number is crucial for anyone involved in banking or financial transactions. This unique nine-digit code is essential for ensuring that money moves smoothly and accurately between banks, especially within the United States. Whether you're setting up direct deposit, making an online payment, or transferring funds between accounts, knowing your bank's routing transit number is vital.

Routing transit numbers (RTNs) are a key component of the banking system's infrastructure. They serve as identifiers for financial institutions, enabling the efficient processing of transactions and maintaining order within the national banking network. With the increasing reliance on electronic transactions, the importance of RTNs has grown, making them a fundamental aspect of modern finance that both individuals and businesses must comprehend.

In this comprehensive guide, we will explore the significance of routing transit numbers, their role in various banking activities, and how they help streamline financial processes. We'll delve into the history and structure of RTNs, how they're used in everyday banking, and provide insights into finding and using them effectively. By the end of this article, you'll have a thorough understanding of routing transit numbers and how they contribute to the seamless operation of the banking system.

Read also:American Giant A Symbol Of Quality And Resilience

Table of Contents

- What is a Routing Transit Number?

- History and Evolution of Routing Transit Numbers

- How Do Routing Transit Numbers Work?

- The Structure of a Routing Transit Number

- Where Can You Find Your Routing Transit Number?

- Importance of Routing Transit Numbers in Banking

- Routing Transit Number vs. Account Number: What's the Difference?

- How to Use Routing Transit Numbers for Transactions

- What Are Common Errors with Routing Transit Numbers?

- Are Routing Transit Numbers Secure?

- Impact of Digital Banking on Routing Transit Numbers

- Routing Transit Numbers and International Transactions

- How to Correct Incorrect Routing Transit Numbers?

- Frequently Asked Questions

- Conclusion

What is a Routing Transit Number?

A routing transit number is a nine-digit code used to identify financial institutions in the United States. It's often used in conjunction with an account number to facilitate the processing of transactions such as direct deposits, wire transfers, and other automated payments. The RTN ensures that funds are directed to the correct bank and account, playing a crucial role in the banking system's efficiency.

Routing transit numbers are primarily used in domestic transactions. They are essential for anyone who engages in activities like setting up automatic bill payments, receiving tax refunds, or transferring funds between different banks. The number is usually found at the bottom of a check or bank statement, along with the account number and check number.

History and Evolution of Routing Transit Numbers

The concept of the routing transit number was first introduced in 1910 by the American Bankers Association (ABA) to streamline the processing of checks. Initially, these numbers were used to identify the bank and branch that issued a check, making it easier for the Federal Reserve and other clearinghouses to manage check processing efficiently.

Over the years, as the banking system evolved and technology advanced, routing transit numbers became an integral part of electronic funds transfer systems. The advent of automated clearinghouses (ACH) and wire transfer networks necessitated the use of RTNs to ensure accurate routing of transactions. Today, they remain a critical component of the banking system, supporting a wide range of financial activities.

How Do Routing Transit Numbers Work?

Routing transit numbers work by providing a standardized way to identify the financial institution responsible for processing a transaction. When you initiate a transaction, the RTN helps the payment system determine which bank will handle the funds. This process ensures that money is sent to the correct destination, minimizing errors and delays in the transaction process.

For example, if you're setting up direct deposit for your paycheck, you'll need to provide your employer with your bank's RTN and your account number. This information allows the payroll system to send your funds to the right bank and account. Similarly, when paying bills online or transferring money between accounts, the RTN is used to direct the transaction correctly.

Read also:Ava Daniels An Illuminating Profile And Unseen Dimensions

The Structure of a Routing Transit Number

A routing transit number consists of nine digits, each serving a specific purpose in identifying the financial institution. Here's a breakdown of the structure:

- The first two digits indicate the Federal Reserve District where the bank is located.

- The next two digits represent the Federal Reserve Bank within that district.

- The fifth digit is a check digit, calculated using a specific formula to ensure the number's validity.

- The last four digits identify the specific bank or branch.

This structured format allows the banking system to process transactions efficiently, ensuring that funds are directed to the correct institution.

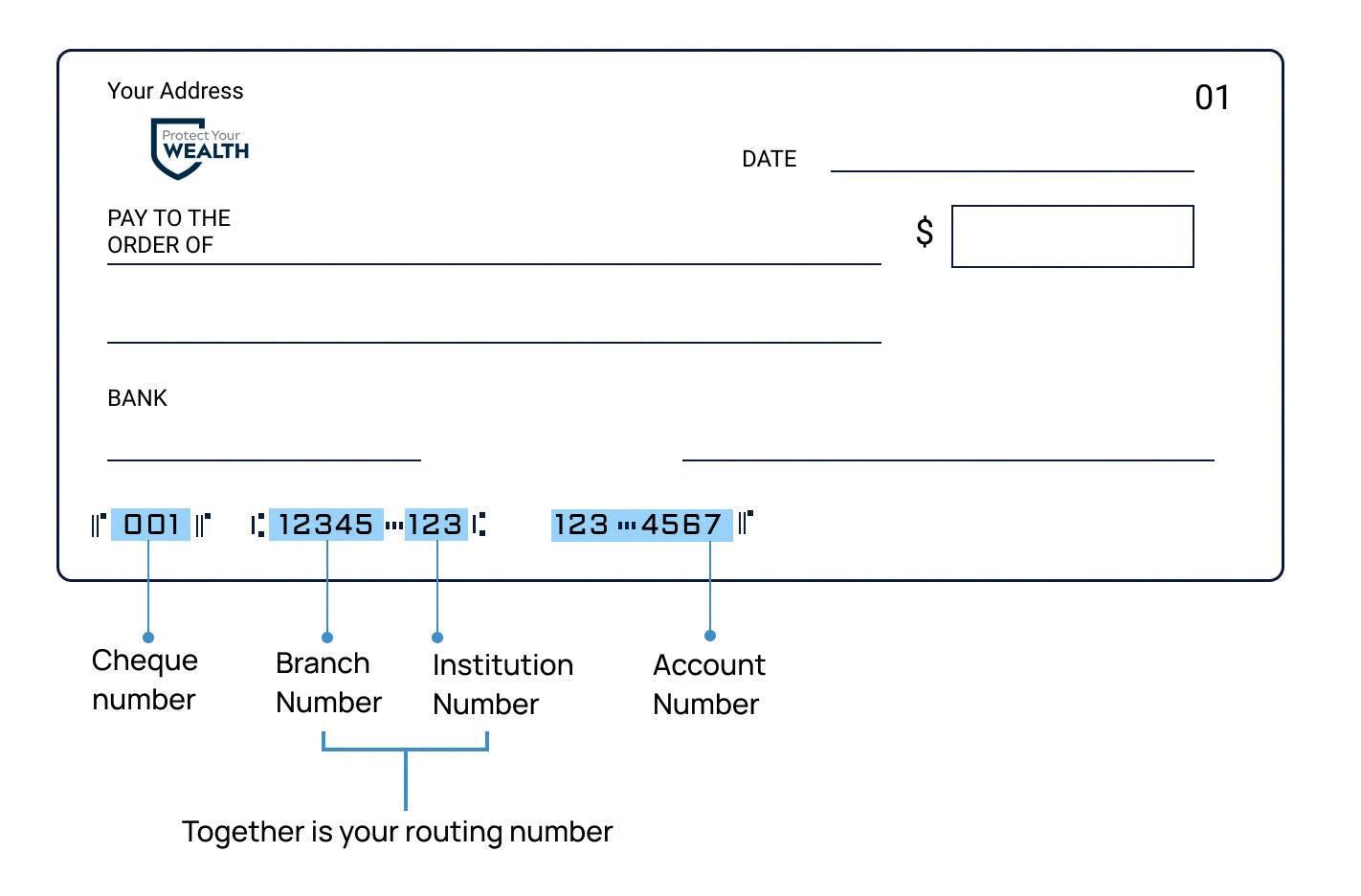

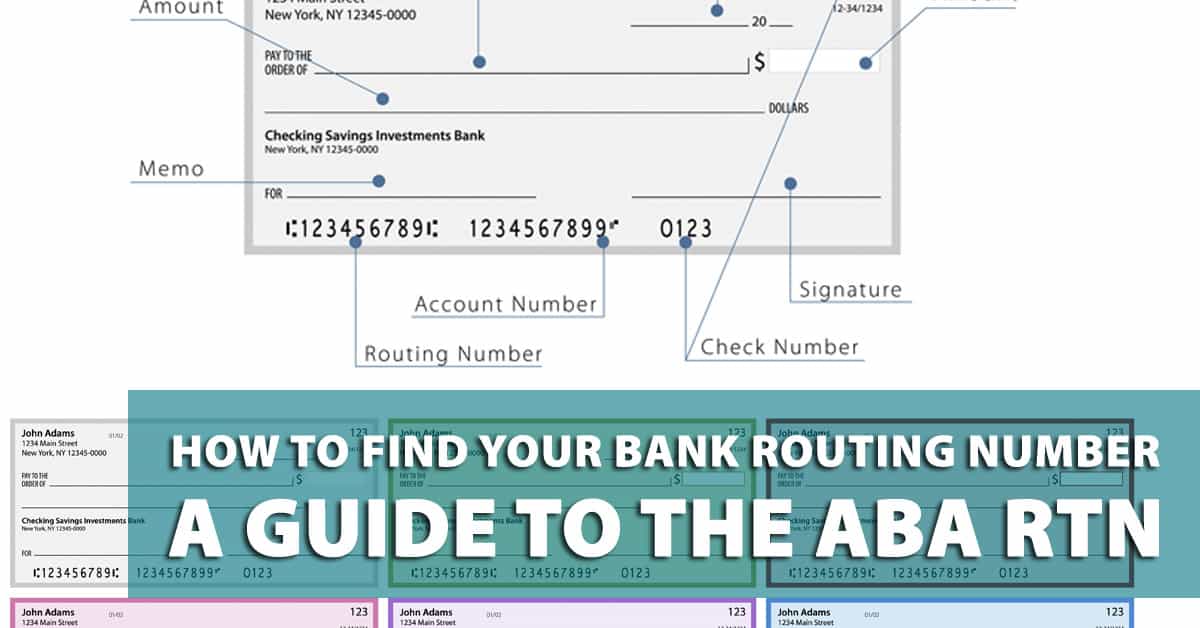

Where Can You Find Your Routing Transit Number?

Your routing transit number can typically be found in several places, depending on your bank and the type of account you have:

- Checks: The RTN is usually printed at the bottom left corner of your checks, followed by your account number and check number.

- Bank Statements: Many financial institutions include the RTN on monthly or quarterly account statements for easy reference.

- Online Banking: You can often find your RTN by logging into your online banking account and navigating to the account details or settings section.

- Mobile Banking Apps: Similar to online banking, mobile apps may display your RTN in the account information section.

- Contacting Your Bank: If you're unsure about your RTN, you can always contact your bank's customer service for assistance.

Knowing where to find your routing transit number is essential for ensuring smooth transactions and avoiding potential delays or errors.

Importance of Routing Transit Numbers in Banking

Routing transit numbers play a vital role in the banking system by facilitating the efficient and accurate processing of transactions. Here are some reasons why they are so important:

- Accuracy: RTNs help ensure that funds are directed to the correct financial institution, minimizing the risk of errors and lost payments.

- Efficiency: By streamlining the routing process, RTNs enable faster processing of transactions, which is especially important in today's fast-paced financial environment.

- Security: Using RTNs adds an additional layer of security to transactions, as the numbers are unique to each bank and branch.

- Standardization: The standardized format of RTNs simplifies the processing of transactions across different financial institutions, promoting consistency and reliability.

Overall, routing transit numbers are a fundamental component of the banking system, supporting a wide range of financial activities and ensuring the smooth operation of domestic transactions.

Routing Transit Number vs. Account Number: What's the Difference?

While both routing transit numbers and account numbers are essential for processing transactions, they serve different purposes and have distinct characteristics:

- Routing Transit Number: As mentioned earlier, the RTN is a nine-digit code used to identify a specific financial institution within the banking system. It ensures that transactions are routed to the correct bank and branch.

- Account Number: An account number is a unique identifier assigned to an individual's or business's bank account. This number differentiates one account from another within the same bank, ensuring that funds are credited to or debited from the correct account.

In summary, the routing transit number identifies the bank, while the account number identifies the specific account within that bank. Both numbers are required for most banking transactions, ensuring that funds are directed accurately and efficiently.

How to Use Routing Transit Numbers for Transactions

Using routing transit numbers for transactions is relatively straightforward, but it's essential to ensure accuracy to avoid delays or errors. Here are some common scenarios where you'll need to use your RTN:

- Direct Deposits: When setting up direct deposit for your paycheck or government benefits, you'll need to provide your employer or the relevant agency with your bank's RTN and your account number.

- Online Payments: When paying bills or making online purchases, you'll often be asked to enter your bank's RTN and your account number to complete the transaction.

- Wire Transfers: For domestic wire transfers, you'll need to provide the recipient's RTN and account number to ensure the funds are sent to the correct bank and account.

- ACH Transfers: Automated Clearing House (ACH) transfers, such as recurring payments for subscriptions or services, require the RTN and account number to process the transaction accurately.

In all these scenarios, double-checking the RTN and account number is crucial to prevent any issues with the transaction.

What Are Common Errors with Routing Transit Numbers?

Despite their importance, errors with routing transit numbers can occur, leading to delays or failed transactions. Here are some common mistakes to watch out for:

- Incorrect RTN: Entering the wrong RTN can result in the funds being routed to the wrong bank, causing delays or lost payments.

- Transposed Digits: Mistakes such as transposing digits in the RTN can lead to incorrect routing and transaction failures.

- Outdated RTN: Banks may change their RTNs due to mergers or reorganizations, so it's essential to ensure you have the most up-to-date number.

- Mixing Up RTN and Account Number: Confusing the RTN with the account number can lead to incorrect information being entered, resulting in failed transactions.

By being vigilant and double-checking the information you provide, you can minimize the risk of errors and ensure smooth transactions.

Are Routing Transit Numbers Secure?

Routing transit numbers are generally considered secure, as they are publicly available and do not provide direct access to your bank account. However, it's essential to use them carefully and responsibly to maintain the security of your financial information.

Here are some tips to enhance the security of your RTN:

- Verify Sources: Only provide your RTN to trusted sources, such as your employer or a reputable business when setting up direct deposits or payments.

- Avoid Sharing Publicly: Do not share your RTN on social media or public forums, as this could expose you to potential fraud.

- Monitor Accounts: Regularly check your bank statements and online accounts for any unauthorized transactions, and report any suspicious activity to your bank immediately.

By following these precautions, you can help protect your financial information and minimize the risk of fraud or unauthorized access.

Impact of Digital Banking on Routing Transit Numbers

The rise of digital banking has transformed the way people access and manage their finances. While the fundamental role of routing transit numbers remains unchanged, digital banking has impacted how they are used and accessed.

One significant change is the increased reliance on online and mobile banking platforms, where users can easily find and use their RTNs for transactions. This convenience has made it easier for individuals to manage their banking needs without visiting a physical branch.

Additionally, digital banking has facilitated the growth of electronic payment systems, such as peer-to-peer payment apps and digital wallets, which often require users to provide their RTN and account number for setup and transactions. This trend has further solidified the importance of routing transit numbers in the modern banking landscape.

Routing Transit Numbers and International Transactions

While routing transit numbers are primarily used for domestic transactions within the United States, they can also play a role in international transactions, albeit indirectly. When sending or receiving money across borders, it's essential to consider additional identifiers, such as SWIFT codes or IBANs, which are used alongside RTNs to facilitate international transfers.

For example, when receiving an international wire transfer, you may be asked to provide your bank's SWIFT code and your account number, in addition to the RTN. These additional identifiers ensure that funds are routed accurately across different countries and banking systems.

It's essential to understand the requirements for international transactions and provide all necessary information to avoid delays or issues with cross-border payments.

How to Correct Incorrect Routing Transit Numbers?

If you realize you've provided an incorrect routing transit number for a transaction, it's crucial to act quickly to minimize any potential issues. Here are some steps to take:

- Contact the Bank or Service Provider: Reach out to the bank or service provider involved in the transaction as soon as possible to inform them of the error. They may be able to correct the mistake before the transaction is processed.

- Monitor the Transaction: Keep a close eye on the transaction's status to ensure it is processed correctly and that no funds are lost or misrouted.

- Request a Reversal: If the transaction has already been processed with the incorrect RTN, you may need to request a reversal or refund from the bank or service provider.

- Update Information: Once the issue has been resolved, ensure that you update your records with the correct RTN to prevent future errors.

By taking prompt action and following these steps, you can help mitigate the impact of incorrect routing transit numbers and ensure the smooth processing of your transactions.

Frequently Asked Questions

What is the purpose of a routing transit number?

The routing transit number serves as an identifier for financial institutions within the United States, facilitating the accurate and efficient processing of transactions like direct deposits, wire transfers, and automated payments.

Can I use my routing transit number for international transactions?

While routing transit numbers are primarily used for domestic transactions, they can be used in conjunction with other identifiers, such as SWIFT codes or IBANs, for international transactions. It's essential to provide all necessary information for cross-border payments.

How do I find my bank's routing transit number?

You can find your bank's routing transit number on checks, bank statements, online banking platforms, mobile apps, or by contacting your bank's customer service for assistance.

What should I do if I enter an incorrect routing transit number?

If you provided an incorrect RTN, contact the bank or service provider immediately to inform them of the mistake. Monitor the transaction and request a reversal if necessary, and update your records with the correct number.

Are routing transit numbers secure?

Routing transit numbers are generally secure, as they do not provide direct access to your bank account. However, it's essential to use them responsibly and avoid sharing them publicly to minimize the risk of fraud.

What is the difference between a routing transit number and an account number?

The routing transit number identifies the bank within the banking system, while the account number identifies the specific account within that bank. Both numbers are necessary for processing most banking transactions.

Conclusion

Routing transit numbers are a fundamental component of the banking system, ensuring the smooth and accurate processing of transactions within the United States. By understanding their purpose and how to use them effectively, individuals and businesses can navigate the complexities of modern finance with confidence.

As digital banking continues to evolve, the importance of routing transit numbers remains undiminished, providing a reliable framework for managing a wide range of financial activities. By staying informed and vigilant, you can maximize the benefits of RTNs and ensure the security and efficiency of your banking transactions.

Article Recommendations